subject: Cash Caches [print this page] Introduction - The Cash Build Up Introduction - The Cash Build Up

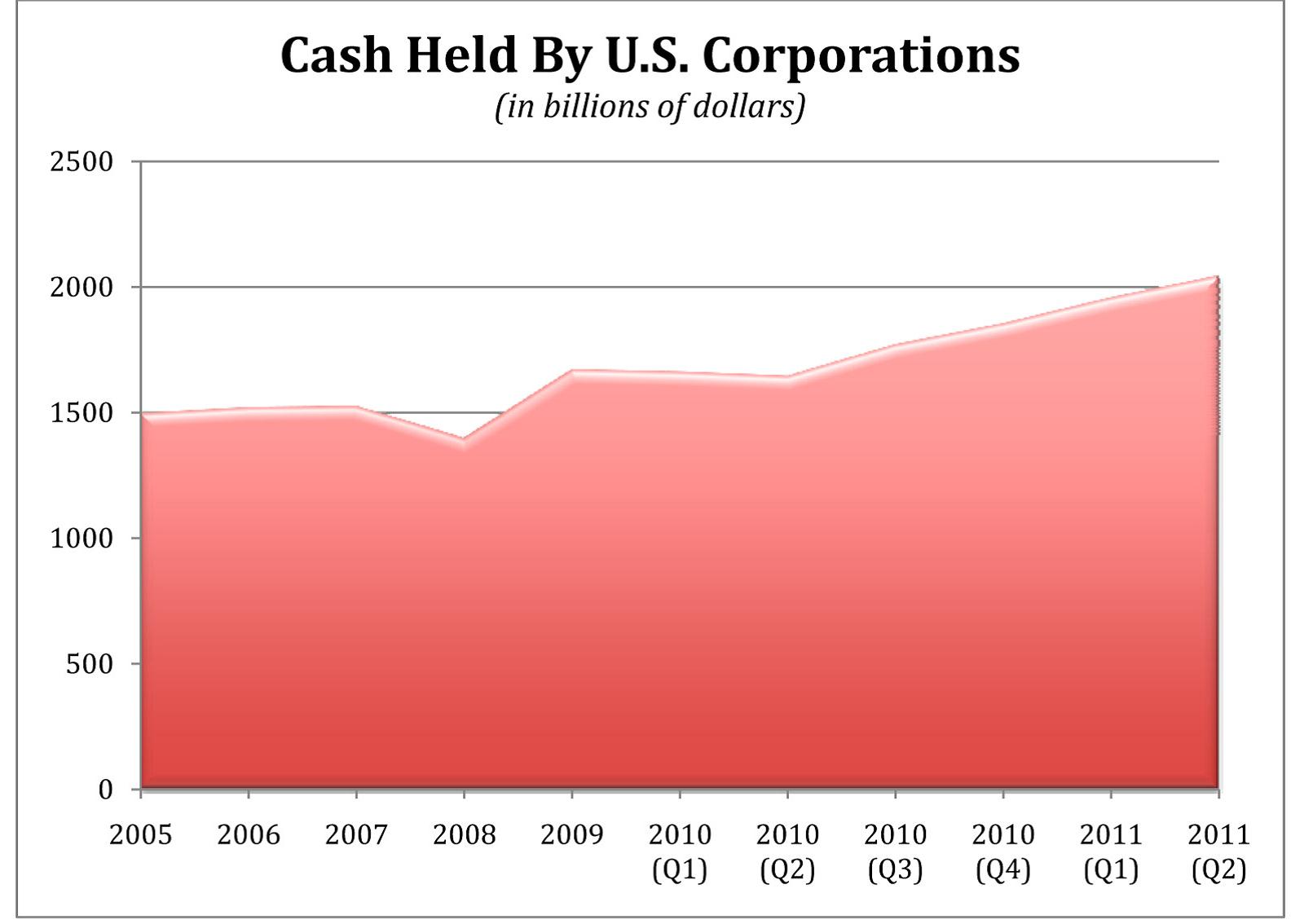

Corporations held a record $2.05 trillion in cash at mid-year 2011. This historically large buffer, which, as the graph below shows, began accumulating beyond norms in 2009 and 2010, can give companies the flexibility to weather another economic downturn and the possibility of attendant funding difficulties.

Interestingly, most of this cash has been generated from operations, which is a positive sign for the health of the corporations amassing it. However, not all of it is the result of sales. It has also been boosted by large amounts of corporate borrowing in the first half of 2011, when companies rushed to take advantage of low rates. Even tech giants with massive overseas cash positions tapped the market to raise funds, rather than suffer the tax hit on repatriated overseas cash. In any case, the $2.05 trillion number is not adjusted for those liabilities.

Even when cash comes strictly from operations, the accumulation is not an unalloyed win for companies, since it reflects corporate inability to invest productively. And, for all the apparent wisdom of saving for a rainy day, the cash build-up has come under scrutiny from equity analysts and investors who are eager to see the monies put to work or returned to shareholders.

The U.S. government, too, is eying the situation, since it is eager to collect the 35 percent in taxes that companies would have to pay if they repatriated cash held outside the country. Since the beginning of the Obama Administration, corporations have been lobbying for a tax holiday on repatriated cash, similar to the Homeland Investment Act of 2004, which lowered the tax rate to 5 percent. However, corporations failed to use the cash repatriated in 2004 in the manner stipulated in the law for research and development and domestic growth initiatives. Instead, they paid most of it out to shareholders, angering legislators and making a repeat of the scheme unlikely.

Apart from taxes, there are opportunity cost and risk management issues involved in holding large amounts of cash, an asset that is neither static nor low-risk. These range from the corrosive effects of inflation in a low interest rate environment to foreign exchange hedging challenges.

Reval expects the aggregate cash on U.S. corporate balance sheets to decline when attractive investment opportunities and economic certainty return. However, financial executives will probably remember the painful liquidity lessons of the financial crisis and keep more cash on hand going forward. That means the total will remain above its normal level for some time.

Part 1: Drawings and Setbacks

While it may seem counterintuitive that a company can suffer from being flush with cash, what are often overlooked are the risks it poses. Excess cash can actually increase risk, offsetting the ostensible benefits of accumulating cash in the first place.

For example, according to an August 24, 2011 article in trade publication, International Treasurer, many companies are changing their investment guidelines to allow their treasury investment managers to invest in higher-risk, and hopefully higher return, instruments. Most have reduced their minimum acceptable rating to BBB; others are considering such a move.

The investments these companies have added to their "acceptable" lists include bank loans, emerging market debt, BBBrated corporates, supranational and sovereign debt, and asset or commercial mortgage-backed securities. Among the asset classes that companies have dropped are prime money market funds and muni bonds.

The principle complications that arise from building a large cash balances include:

1. Banking costs. Banks may begin to charge fees on cash holdings above certain levels. Bank of New York Mellon (BONY) last summer became the first to announce such a move, saying it would charge 13 basis points on balances of $50 million or more.

This fee is driven by banks increased collateral necessities and FDIC requirements mandated by legislation, as well as the simple difficulty faced by bank treasurers looking to put the deposits to work in positive-return short-term investments.

Other banks may not follow BONY's lead, since bankers traditionally see deposits as a cheap source of stable funding, and one that will help them meet Basel III liquidity requirements. This may offset the cost of managing the funds, especially when the value of client relationships is added to the mix. Nonetheless, BONY's move has been a major source of uncertainty.

2. Visibility and hedging. Generating and maintaining large international cash balances raises the importance of cash visibility and FX hedging. Large international banks have begun to offer centralized, high-visibility, cash management programs that automatically zero-out balances of overseas subsidiaries at the end of each day and hedge the net amount. Having a best of breed in-house system for managing FX risk remains crucial to managing and executing these programs, since companies have to keep close tabs on the banks managing these programs.

3. Counterparty risk. The bankruptcy of Lehman Brothers, the Reserve Fund's subsequent breaking of the buck, and the run on money funds in the wake of those events demonstrated the importance of managing the counterparty risk of the institutions where corporate cash is deposited or invested. Diversification by institution and geography is crucial, as is having solid processes and tools to assess counterparty risk. As the ratings agencies' performance regarding Lehman Brothers demonstrated, relying on third party credit analysts is not sufficient.

4. Banks' dwindling options. Basel III is forcing banks to collateralize their cash holdings. This is driving banks to limit cash and fund investment options. Limiting options will ultimately drive down yields or even push corporations toward non-stable investment options.

5. Tax considerations. Despite ongoing lobbying for a "Homeland Investment Act 2.0," in the U.S. companies should not make their plans contingent on a tax holiday. While many developed countries, such as Japan and the U.K., have territorial tax systems, which leave overseas profits to be taxed in the jurisdictions in which they are generated, the U.S. has not

followed suit. That means cash held overseas by U.S. companies remains subject to a 35 percent tax rate, if repatriated to the U.S. Companies have issued debt to avoid this even to fund dividends and buybacks making it slightly less attractive to keep the cash abroad. But as long as rates stay low, there will be little impetus to bring the cash home.

Part Two: Benefits and Opportunities

While the risks of accumulating cash are often overlooked, the benefits are more obvious:

1. Cash is deemed as safe. Most other investments now appear risky. For example, even low-risk money market funds, recently subjected to new, stricter Securities and Exchange Commission investment rules, are seen as hazardous. Corporations pulled over $70 billion from the funds during first week of August on jitters about the European sovereign debt crisis.

2. Cash creates resiliency. Strong cash holdings allow a corporation to weather another economic downturn by ensuring access to capital.

3. Cash can fund operations. Cash allows a corporation to grow through capital expenditures investing back in the business.

4. Cash can fund M&A. Cash-rich companies do not have to rely on the capital markets to fund acquisitions.

5. Cash can raise dividend yields. If a company does not have attractive business investments on the horizon, it can pay out the cash to shareholders.

6. Cash deleverages. It lowers a company's weighted average cost of capital and allows companies to pay down debt.

7. Cash boosts capital market access. Conversely, high cash levels increase a company's creditworthiness thus allowing a corporation to borrow more and at lower costs. Many corporations are taking advantage of this by increasing their borrowing alongside increases in cash holdings. Ultimately this strategy is geared toward preservation of capital during a major downturn.

8. Cash offers operational flexibility. High cash levels enable a company to take a closer look at working capital processes. Opportunities may exist for more favorable terms and discounts with suppliers. Receivable management can be looked at to as many of a company's customers are holding excess cash.

Part 3: Best Practices

Despite the obvious benefits and risks around cash, the assumption that cash is a static and low-risk asset is often to blame for companies not pursuing best-in-class cash management. When cash balances are low, or a company has not yet evolved from a domestic operation to an international venture, that assumption might not be a problem. However, once a company's business begins to cross borders, and cash balances rise, a "benign neglect" approach is no longer appropriate.

Top issues include:

1. Know your cash. You can't manage what you don't know. Know how much cash you have, what currency it is in and what counterparty holds it. Companies with best-in-class cash management operations work hard to achieve cash visibility, ensuring the banks they use can feed data into their systems as needed. They know what their foreign exchange exposure is at all times, and have established mechanisms for hedging or moving cash positions as developments call for it.

2. Investigate netting options. Large international banks provide daily cash netting and zero-balance services. These can be customized to suit a company's specific needs. They vary in approach and scope, so they should be evaluated carefully.

3. Adopt 21st Century FX hedging strategies. Examine, or re-examine, your FX hedging strategy. It may be out of date. The first and most important step in developing a financial risk management and hedging strategy is knowing exactly what and where your exposures are and determining what your tolerance for this risk is.

Many treasurers and financial executives put so much focus on deciding how to hedge that sufficient attention has not been allocated to understanding their exposures. The first principle of effective hedging is accurately measuring and understanding exposures and understanding how hedging or not hedging will impact a firm's ability to deliver on their business plan.

From there, you can think about what and how to hedge. Make sure data sources, trading platforms and back office operations are up to speed. Then, do it all again. Evaluate your strategies and hedge performance so that you can make adjustments to your strategy. Risk constantly arises in new shapes and forms. Best practice frameworks for financial risk are a constant, revolving business process.

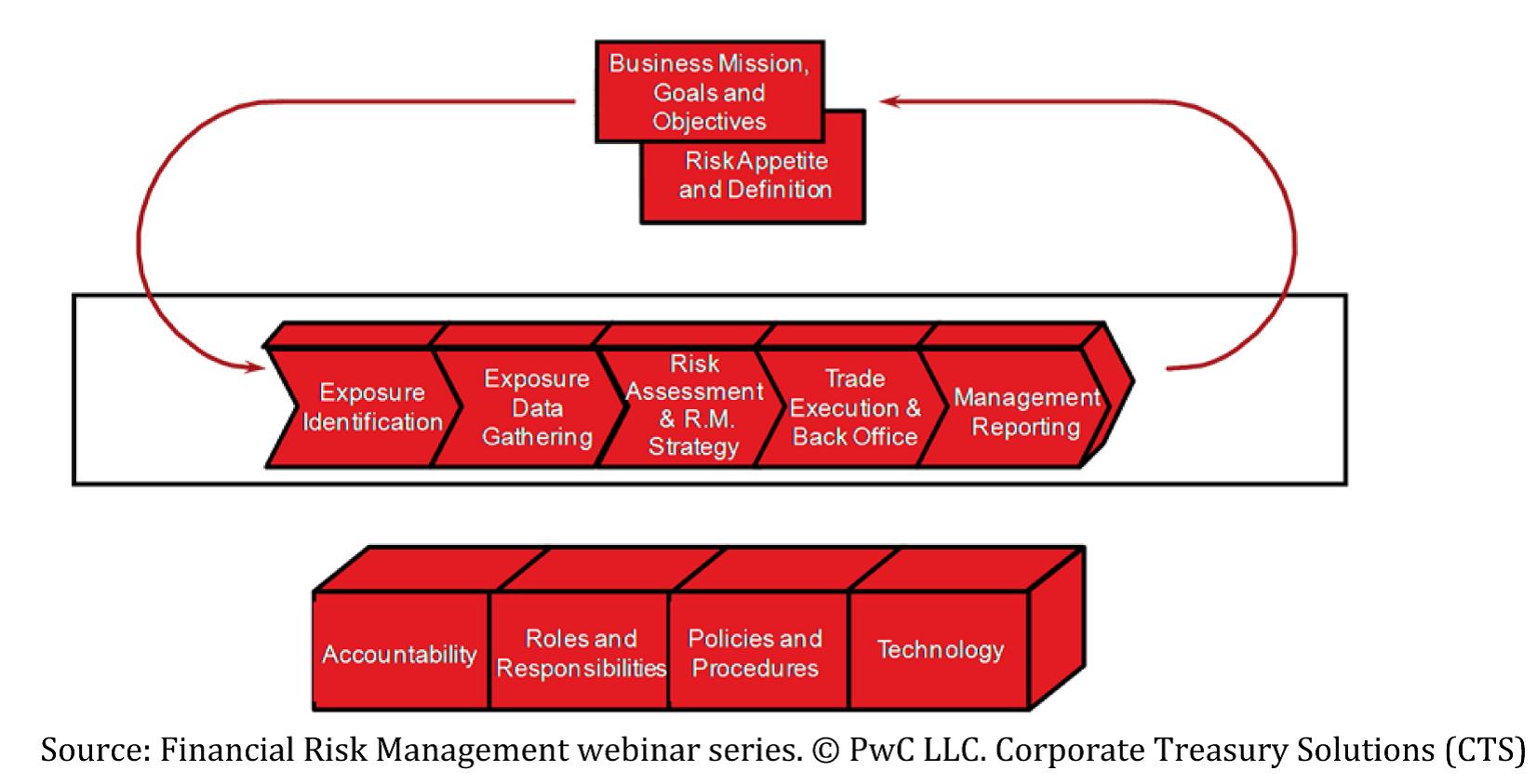

Diagram: PwC best practice financial risk management framework:

4. Cash flow forecasting. This has always been and will continue to be a hot topic for treasurers and CFOs. Executing and delivering an accurate and confident cash flow forecast involves six key disciplines:

Top down initiative. Senior executives need to mandate forecast performance and identify to key staff the strategic value of forecasting for the organization. Otherwise, forecasting will be seen as too burdensome and staff will just go through the motions.

Identify the best data sources. Garbage in delivers garbage out. It's crucial that an organization identifies the most relevant data sources to acquire the inputs to the forecast. Common areas include: Subsidiary/business unit forecasts, maturities of financial instruments, historical actual transactions, system imports such as accounts receivable and payable, budget systems, payroll, and so on.

Automate the consolidation of these data sources. Organizations often spend too much time just trying to bring this information together. This leaves no time for validation and analysis. Automation from many to one is key.

Reconciliation and performance testing. Creating a forecast is just the first step. Forecast adjustments are critical and can only be done effectively with good intelligence into how your forecasting compared with what actually happened. Improvements can only be made when you realize what factor moved against you. About 80 percent of the time dedicated to forecasting should be spent on forecast accuracy testing and adjustments.

Scenario testing. After you've checked your forecasts against actuals and have honed the process, it is time to run scenarios. This enables the organization to understand and plan for situations that may arise in the future. Common scenarios used by world-class forecasters include: FX shifts, interest rate shifts, best case/worst case shifts, adjustment up or down by a given percent, and shocking large inflow or outflows of the forecast.

Retain talent. Turnover within your cash management operations can cripple your decision making. Cash operations are a combination of art and science. A staff exodus can seriously jeopardize confident execution.

Recently, Reval provided the technology for one company's FX systems revamp, and, in the context of an overall FX business process re-engineering, achieved the following goals for the client:

- Streamlined FX hedging processes and better met SOX and GAAP requirements.

- Maintained portfolios for each hedge program, with the flexibility to break down, group,

consolidate, and zoom in and out.

- Looked at exposures and hedges over different time horizons.

- Stress tested and ran scenario planning for risk evaluation purposes.

- Used new tools to hedge business risk, including options.

- Evaluated different hedging strategies and ran simulations in parallel for benchmarking.

- Provided meaningful and accurate reporting to senior management.

The important steps this company has taken has ensured it is now better prepared for future challenges.

Conclusion

Building and holding large reserves of cash has been a central tenant of post-financial crisis strategy for many companies. However, as this white paper states, cash is neither a static or risk-free asset. Whether it is the risks associated with banks, or regulation, or FX, cash can easily turn from asset to headache.

As economic uncertainty continues to swirl around global markets, companies are likely to maintain their cash reserves, and rely on them heavily should a double dip recession strike.

Assessing the opportunities and risks of deploying or holding cash requires a high degree of visibility as well as best-in-class risk management tools. Without the ability to clearly see where cash sits across an enterprise, CFOs and treasurers cannot maximize the effectiveness and value of cash as an asset.

Today, the record amount of cash building up in different divisions of many corporations is matched by the level of risk associated with all that cash. The need for a greater level of visibility into these cash positions is greater than ever.